Learn how banking systems work, including deposits, loans, interest rates, and financial services. A complete guide to understanding modern banking systems.

Introduction

Most of us interact with banks almost every day—whether it’s checking a balance on a mobile app, transferring money, paying bills, or receiving a salary deposit. Yet surprisingly, very few people truly understand how banking systems actually work.

Where does the money go after you deposit it?

How do banks earn profits from loans?

And why do banks play such a critical role in the economy?

These questions sit at the heart of modern finance.

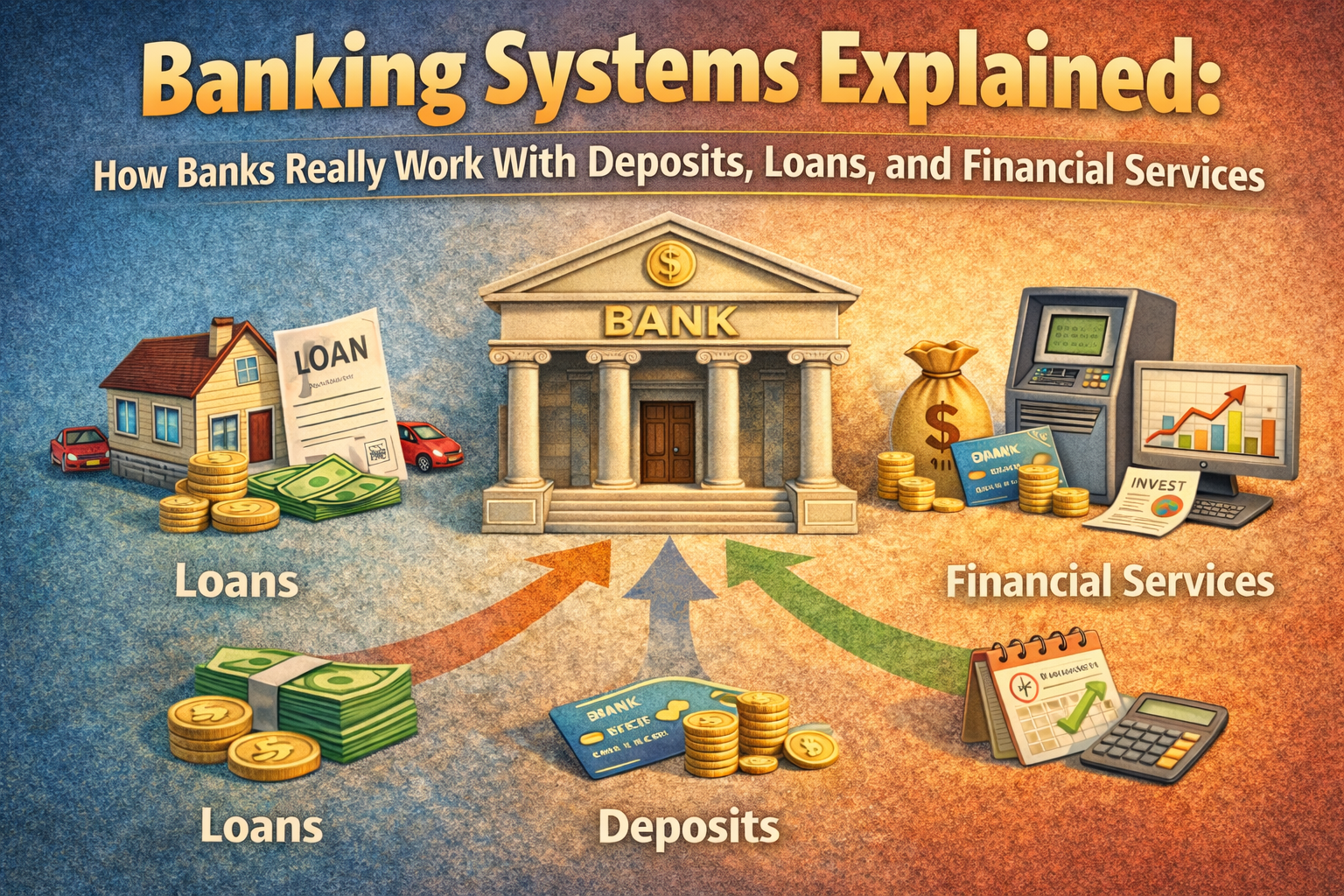

Banking systems refer to the structure and processes through which banks operate to manage deposits, provide loans, facilitate payments, and deliver financial services to individuals, businesses, and governments.

Banks act as financial intermediaries, connecting people who want to save money with those who need to borrow it. Without them, the global economy would struggle to function efficiently.

Understanding how banking systems work can help you make better decisions about saving, borrowing, investing, and managing money overall.

Let’s break down how banks operate behind the scenes.

What Are Banking Systems?

A banking system is a network of financial institutions that provide services such as:

- Accepting deposits

- Issuing loans

- Processing payments

- Facilitating investments

- Managing financial transactions

Banks essentially move money through the economy while ensuring funds remain safe and accessible.

Most modern economies rely on two main levels of banking institutions:

- Central banks

- Commercial banks

Each plays a different role in maintaining financial stability.

For a broader explanation of how banking systems function globally, you can explore this overview on Wikipedia:

https://en.wikipedia.org/wiki/Banking

The Role of Banks in the Economy

Banks do much more than simply store money.

They help keep the financial system running smoothly by performing several key functions.

1. Safeguarding Deposits

Banks provide a secure place for individuals and businesses to store money.

Deposit accounts include:

- Savings accounts

- Current accounts

- Fixed deposits

- Certificates of deposit

Customers earn interest on some of these accounts while maintaining easy access to funds.

2. Providing Loans and Credit

One of the most important roles of banking systems is lending money.

Banks provide credit to individuals and businesses for various purposes.

Examples include:

- Home loans (mortgages)

- Personal loans

- Business loans

- Auto loans

- Credit cards

Loans help finance large purchases and fuel economic growth.

3. Facilitating Payments

Banks enable millions of financial transactions every day.

Payment services include:

- Debit card payments

- Online transfers

- Mobile banking

- Automated clearing systems

- International wire transfers

These services make everyday commerce possible.

4. Supporting Economic Growth

By providing access to credit and managing financial transactions, banks help businesses expand and consumers spend.

This circulation of money drives overall economic development.

Types of Banks in a Banking System

Banking systems typically include several different types of financial institutions.

Each serves a unique purpose.

Central Banks

Central banks sit at the top of the financial system.

Examples include:

- The Federal Reserve (United States)

- The European Central Bank

- The Reserve Bank of India

Central banks are responsible for:

- Controlling monetary policy

- Managing inflation

- Regulating the money supply

- Supervising commercial banks

They also set benchmark interest rates, which influence borrowing and lending across the economy.

You can learn more about central banking from the Bank for International Settlements:

https://www.bis.org/about/banking.htm

Commercial Banks

Commercial banks are the institutions most people interact with.

Their main services include:

- Accepting deposits

- Issuing loans

- Providing checking accounts

- Offering credit cards

- Processing payments

These banks operate for profit and generate revenue primarily through interest on loans.

Investment Banks

Investment banks focus on large financial transactions and corporate finance.

Their services include:

- Mergers and acquisitions advisory

- Stock and bond issuance

- Institutional investment management

Unlike commercial banks, they typically do not handle everyday consumer deposits.

Cooperative and Community Banks

These banks serve specific communities or member groups.

They often focus on local lending and small business support.

Examples include credit unions and cooperative banks.

How Banks Make Money

Many people wonder how banks generate profits when they appear to simply hold money.

The answer lies in interest and financial services.

Banks typically earn money through:

1. Interest Rate Spread

Banks pay depositors a small interest rate on savings accounts.

They then lend that money at a higher interest rate.

The difference between these two rates is called the interest spread, which generates profit.

2. Loan Interest Payments

Loans generate consistent income through interest payments.

For example:

- Mortgage interest

- Personal loan interest

- Credit card interest

These payments represent a major portion of banking revenue.

3. Service Fees

Banks also earn money through fees such as:

- ATM charges

- Account maintenance fees

- Foreign transaction fees

- Late payment penalties

While individually small, these fees add up significantly.

4. Investment Activities

Some banks invest in financial markets, bonds, and other securities to generate additional returns.

Fractional Reserve Banking: The Hidden Mechanism

One of the most important concepts in modern banking systems is fractional reserve banking.

This system allows banks to lend out a portion of deposited money while keeping a fraction in reserve.

For example:

If you deposit ₹10,000 into a bank:

- The bank may keep ₹1,000 in reserve

- The remaining ₹9,000 can be loaned to borrowers

This process expands the money supply and stimulates economic activity.

A detailed explanation of this system can be found here:

https://en.wikipedia.org/wiki/Fractional-reserve_banking

Modern Banking Services

Today’s banking systems offer far more than traditional deposit and loan services.

Technology has transformed the industry significantly.

Modern services include:

Digital Banking

Customers can now manage accounts entirely through mobile apps and online platforms.

Common features include:

- Instant fund transfers

- Mobile check deposits

- Spending analytics

- Budget tracking tools

Wealth Management

Many banks offer financial advisory services such as:

- Investment planning

- Retirement planning

- Portfolio management

Business Banking

Banks also provide services tailored for businesses, including:

- Payroll management

- Business loans

- Merchant payment solutions

International Banking

Global banks enable cross-border transactions and currency exchange.

This allows businesses and individuals to operate in international markets.

Risks and Regulation in Banking Systems

Because banks hold large amounts of public money, strong regulation is essential.

Governments and regulatory bodies supervise banking activities to maintain stability.

Common regulatory measures include:

- Capital reserve requirements

- Liquidity rules

- Consumer protection regulations

- Deposit insurance systems

These safeguards help prevent bank failures and protect customers.

For example, many countries offer deposit insurance programs that guarantee a certain amount of savings if a bank fails.

Real-Life Example: How Your Deposit Supports the Economy

Imagine you deposit ₹50,000 into your savings account.

The bank may use a portion of that money to:

- Provide a loan to a small business owner

- Finance a home mortgage

- Support a car loan for another customer

Those borrowers then spend money in the economy, creating jobs and business growth.

In this way, banking systems quietly support everyday economic activity.

Conclusion

Banking systems form the backbone of modern economies. They connect savers with borrowers, facilitate payments, provide credit, and support economic growth.

While most people simply see banks as places to store money, their role extends far beyond that.

By managing deposits, issuing loans, and offering financial services, banks keep money moving through the financial system.

Understanding how banking systems work can help individuals make better decisions about saving, borrowing, and managing personal finances.

The more you understand the structure behind banking, the more confidently you can navigate your financial future.

Frequently Asked Questions (FAQ)

What is a banking system?

A banking system is a network of financial institutions that manage deposits, provide loans, facilitate payments, and deliver financial services within an economy.

What are the main functions of banks?

Banks accept deposits, provide loans, process financial transactions, and offer services such as credit cards, investments, and wealth management.

How do banks make money?

Banks earn money through loan interest, service fees, investment activities, and the difference between interest paid on deposits and interest charged on loans.

What is fractional reserve banking?

Fractional reserve banking is a system where banks keep a portion of deposits as reserves and lend the remaining funds to borrowers.

What is the difference between central banks and commercial banks?

Central banks regulate the financial system and control monetary policy, while commercial banks provide everyday banking services like deposits and loans.

Why are banks important to the economy?

Banks support economic growth by facilitating financial transactions, providing credit, and ensuring money circulates efficiently within the economy.