Learn how mortgage rates affect home prices in the U.S. housing market. Discover why rising mortgage rates can impact home prices, buyer demand, and housing affordability.

How Mortgage Rates Affect Home Prices

The relationship between mortgage rates and home prices is one of the most important factors shaping the housing market. Mortgage rates influence how much buyers can afford to borrow, which directly impacts demand for homes. When mortgage rates change, home prices often react accordingly.

In the United States housing market, millions of buyers rely on mortgage loans to purchase property. Because most homebuyers finance their purchases through mortgages, changes in interest rates can significantly influence home prices.

Understanding how mortgage rates affect home prices helps buyers, investors, and policymakers make better financial decisions. It also explains why housing markets sometimes experience rapid price increases or sudden slowdowns.

The Basic Relationship Between Mortgage Rates and Home Prices

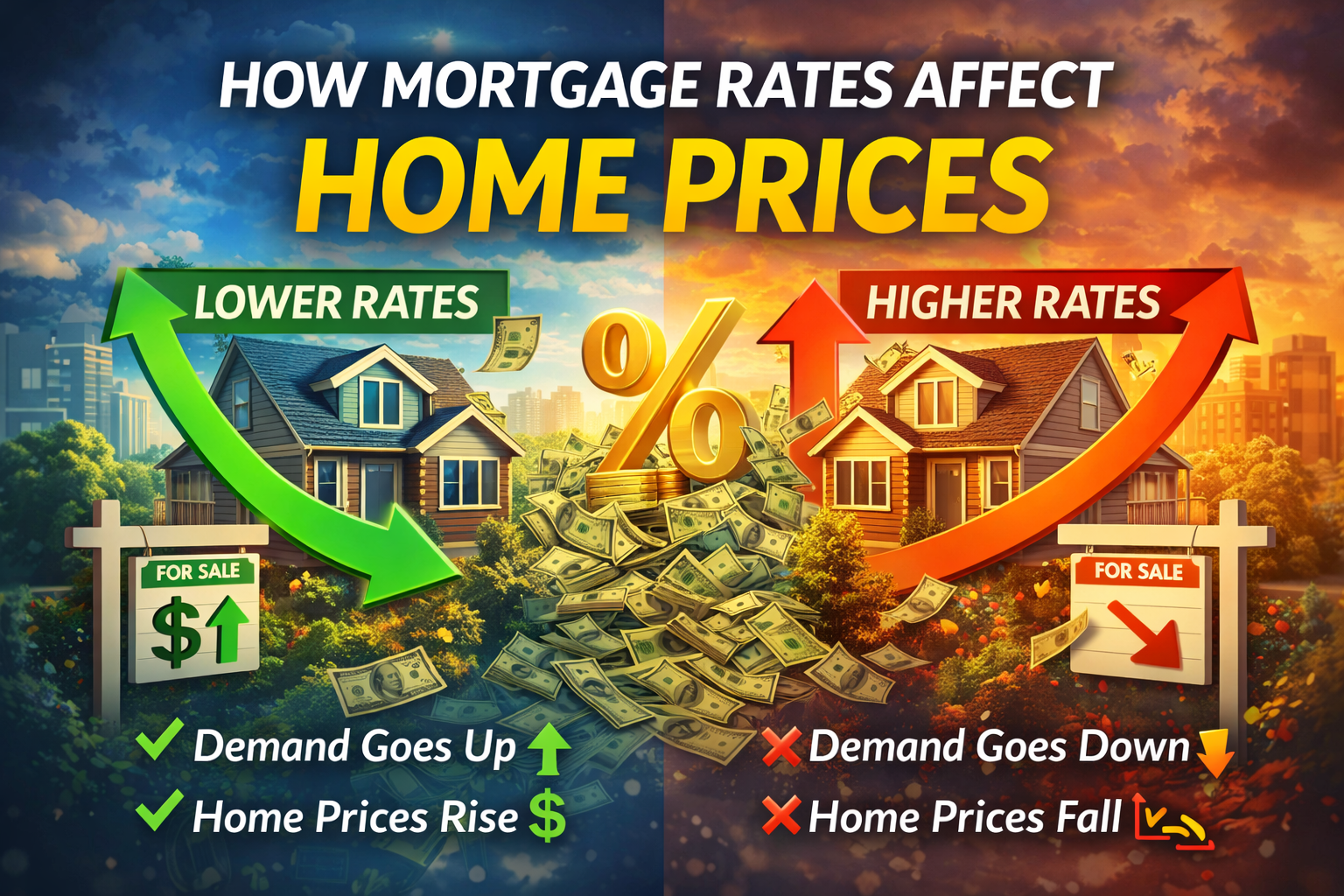

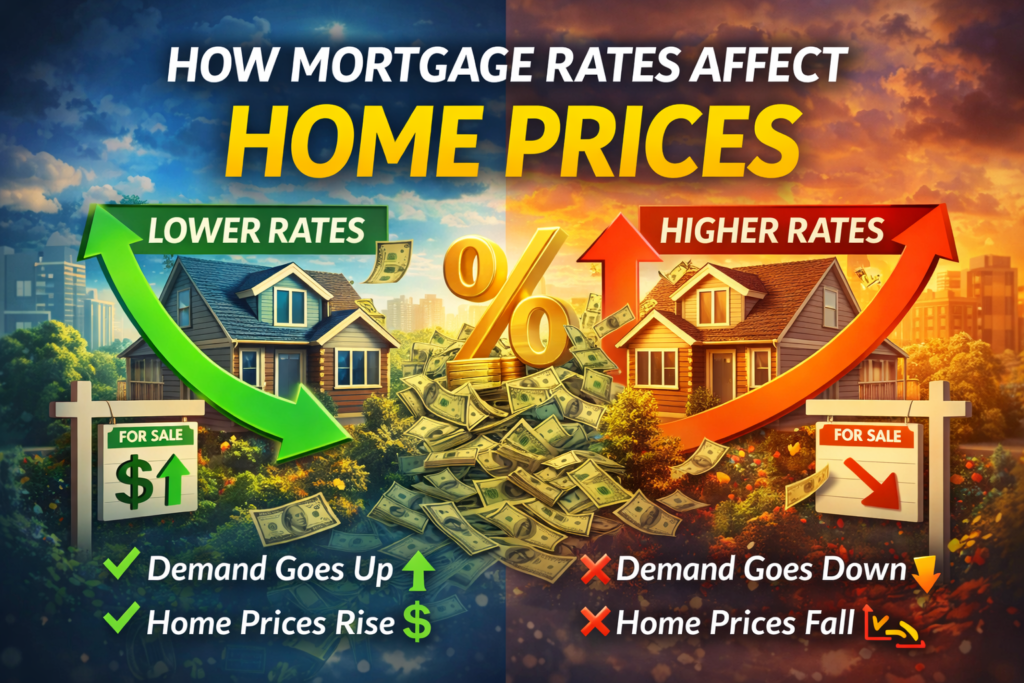

Mortgage rates represent the interest charged by lenders on home loans. When mortgage rates increase, borrowing becomes more expensive. This higher cost reduces purchasing power for many buyers, which can influence home prices.

For example, when mortgage rates rise, the monthly payment required to purchase a home also increases. As a result, some buyers may no longer be able to afford certain properties. This reduced demand can put downward pressure on home prices.

On the other hand, when mortgage rates fall, borrowing becomes cheaper. Lower monthly payments allow more buyers to enter the housing market, which can increase competition for homes. Increased demand often leads to higher home prices.

Economic data and mortgage trends are often tracked by organizations such as the Federal Reserve, which plays a key role in influencing interest rates.

You can learn more about mortgage trends here:

https://www.federalreserve.gov

How Rising Mortgage Rates Reduce Demand for Home Prices

One of the most common effects of rising mortgage rates is reduced housing demand. When borrowing becomes more expensive, many potential buyers delay their purchase decisions.

Higher monthly payments mean that fewer buyers qualify for mortgages. As demand decreases, sellers may have to lower home prices to attract buyers.

For example, if mortgage rates increase from 3% to 7%, the monthly cost of a home loan can increase dramatically. This reduces the number of buyers who can afford certain properties, which can slow growth in home prices.

Housing market research from the National Association of Realtors regularly analyzes how interest rate changes influence home prices.

More information can be found here:

https://www.nar.realtor

How Lower Mortgage Rates Increase Home Prices

Lower mortgage rates often lead to stronger housing demand. When borrowing becomes cheaper, buyers can afford larger loans and more expensive homes.

As more buyers enter the market, competition for available properties increases. This higher demand often pushes home prices upward.

For instance, during periods of historically low mortgage rates, many buyers rush to purchase homes before rates increase again. This surge in demand can cause rapid increases in home prices, especially in high-demand cities.

Data from the Mortgage Bankers Association shows that housing demand often rises significantly when mortgage rates fall.

You can explore mortgage data here:

https://www.mba.org

The Role of Housing Supply in Home Prices

While mortgage rates play a major role, housing supply is another important factor affecting home prices.

If housing supply is limited, home prices may continue rising even when mortgage rates increase. This happens because there are simply not enough homes available to meet buyer demand.

Many major cities in the United States face housing shortages due to population growth, zoning regulations, and limited land availability. These shortages contribute to rising home prices even during periods of higher borrowing costs.

Research conducted by the Harvard Joint Center for Housing Studies highlights the impact of housing supply on home prices.

Learn more here:

https://www.jchs.harvard.edu

Investor Activity and Home Prices

Real estate investors also play an important role in influencing home prices. Investors often purchase properties to generate rental income or long-term appreciation.

When mortgage rates are low, investors can borrow money at cheaper rates, making property investments more attractive. Increased investor activity can drive up home prices, particularly in popular housing markets.

However, when mortgage rates rise significantly, investors may slow down their property purchases. This reduced investment demand can contribute to slower growth in home prices.

Institutional investors and large real estate firms monitor mortgage trends closely because these changes directly affect home prices and market opportunities.

Regional Differences in Home Prices

Mortgage rates affect home prices differently depending on the region. Housing markets in major metropolitan areas often respond differently compared to smaller cities or rural areas.

For example, cities with strong job markets and population growth may continue experiencing rising home prices even during periods of higher interest rates. Meanwhile, markets with slower economic growth may see declining home prices when borrowing costs increase.

Local economic conditions, employment opportunities, and population trends all influence how mortgage rates affect home prices in different regions.

Understanding these regional differences is essential for investors and homebuyers evaluating housing market opportunities.

Long-Term Impact of Mortgage Rates on Home Prices

Although mortgage rates can influence short-term changes in the housing market, home prices are also affected by long-term economic trends.

Population growth, wage increases, housing construction, and government policies all play a role in shaping home prices over time.

Even when mortgage rates rise temporarily, strong economic growth and housing shortages can still support long-term increases in home prices.

For this reason, many real estate experts encourage buyers to consider long-term market trends rather than focusing solely on short-term interest rate fluctuations.

Conclusion

Mortgage rates and home prices are closely connected within the housing market. When mortgage rates rise, borrowing becomes more expensive, reducing demand and potentially slowing growth in home prices. When mortgage rates fall, lower borrowing costs encourage more buyers to enter the market, often pushing home prices higher.

However, mortgage rates are only one factor affecting home prices. Housing supply, investor activity, economic growth, and regional demand also play important roles.

Understanding how mortgage rates influence home prices can help buyers, investors, and policymakers navigate the complex housing market more effectively.

As economic conditions continue to evolve, monitoring mortgage trends will remain essential for predicting future movements in home prices and housing affordability.

The Next Commodity Supercycle: Why Metals and Resources May Dominate the Next Decade : Is a new commodity supercycle coming? Discover why metals, critical minerals, and natural resources may dominate financial markets over the next decade.